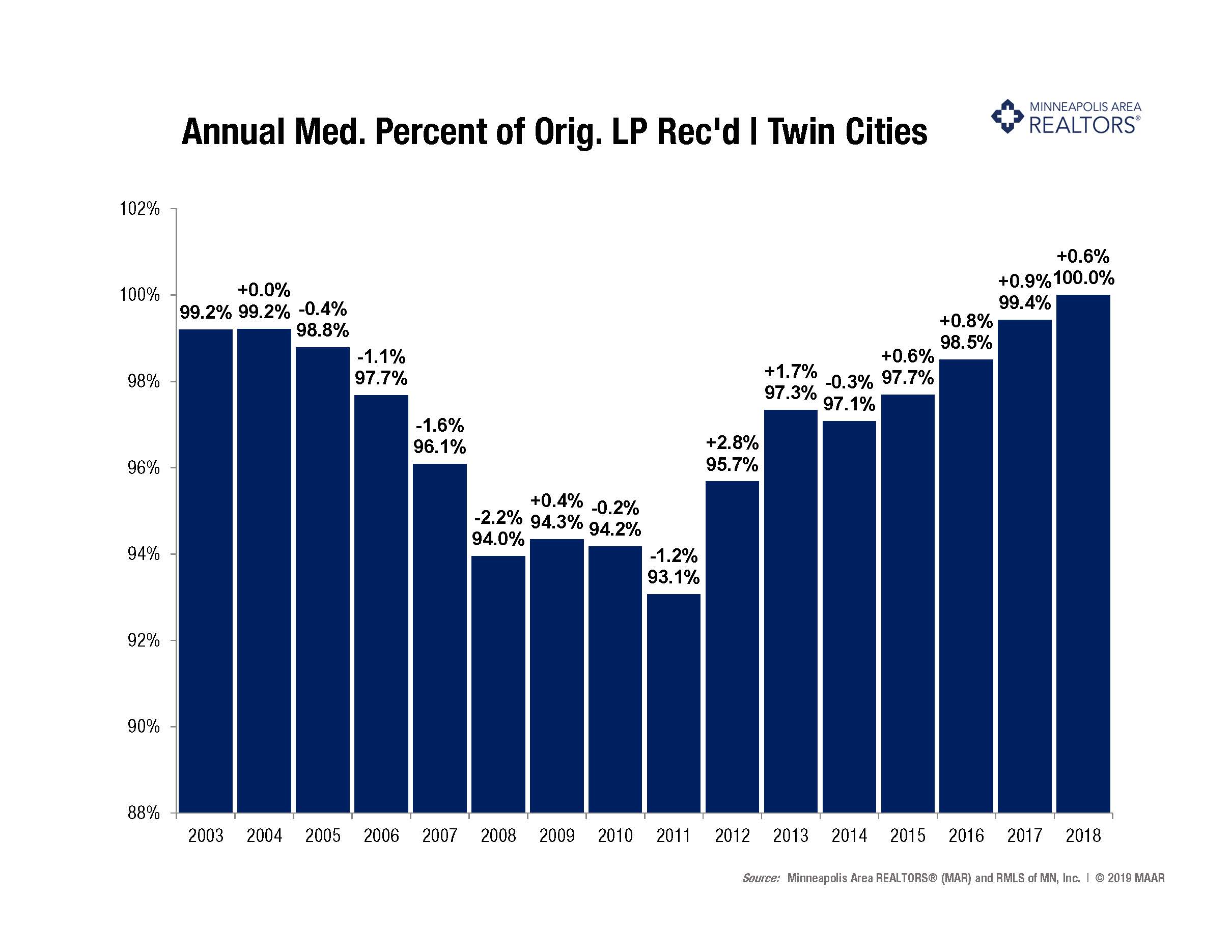

If February was the month of record snowfall, March was the month of record wet basements. The effects of extreme weather continue to impact the market. Despite that, the latest numbers for Twin Cities residential real estate show some strength amidst ongoing signs of change. Prices continued to climb, reaching a new record. New listings fell 8.8 percent as fewer sellers listed their properties. Closed sales were down 9.3 percent as some buyers waited on soggy properties as well as additional inventory options. Market times rose year-over-year for the first time since March 2015. Another sign of a changing market is the ratio of sold to list price has fallen for four of the last five months. This—along with other indicators—suggest the market is improving for buyers, even though sellers still have strong pricing power, favorable negotiating leverage and quick market times.

The number of active listings for sale decreased compared to the prior year. Even so, buyers have seen inventory gains for five of the last six months. Months supply, however, was flat at 1.8 months, suggesting the market is still tight but realigning. Buyers should still expect competition on the most coveted listings. After touching 5.0 percent in November, mortgage rates have settled back down around 4.1 percent, which is great news for buyers. The supply squeeze is most evident at the entry-level prices, where multiple offers and homes selling for over list price are commonplace. The move-up and upper-bracket segments are less competitive and better supplied.

March 2019 by the Numbers (compared to a year ago)

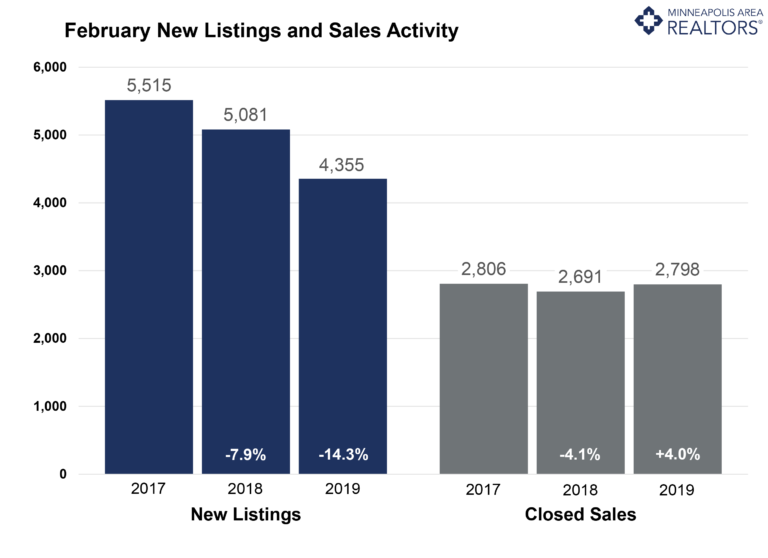

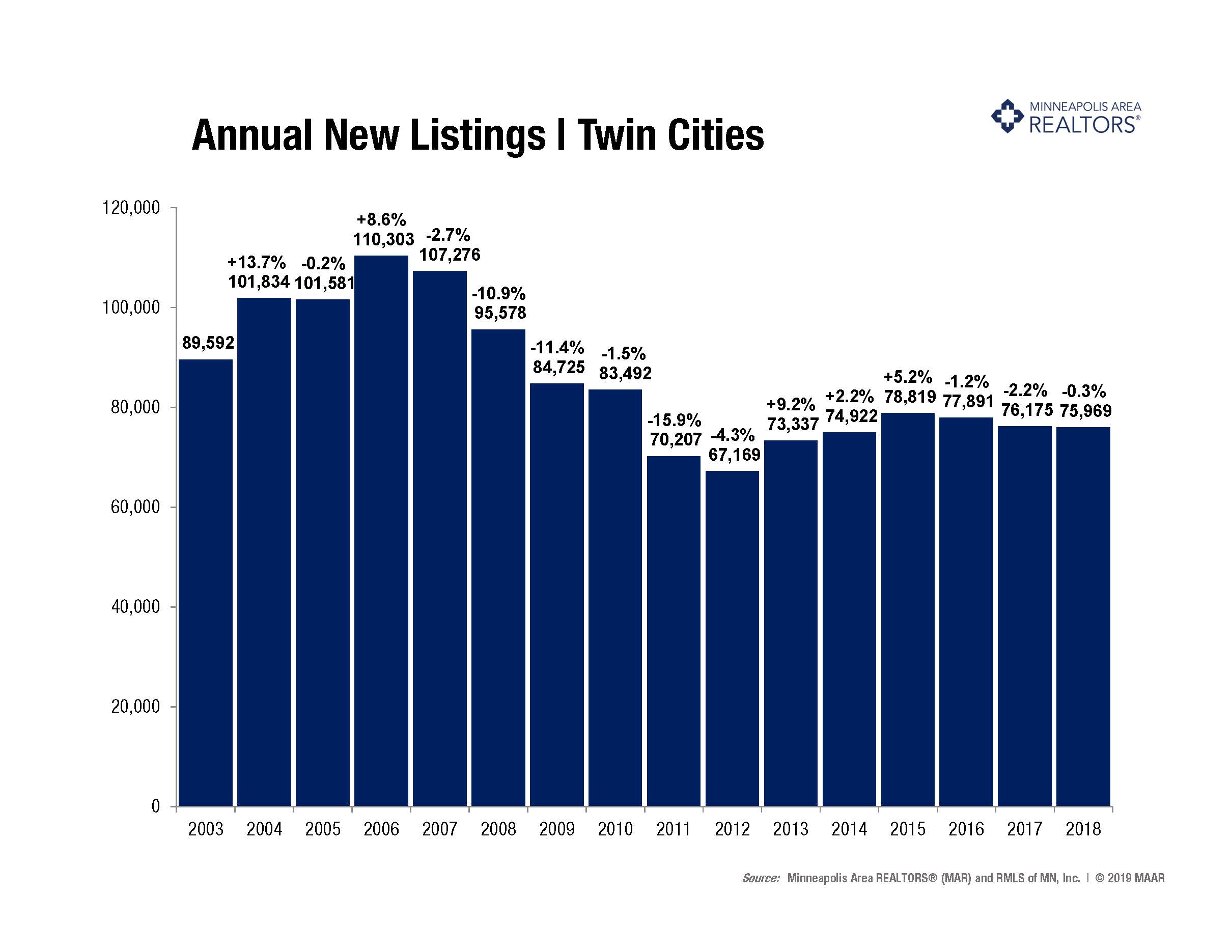

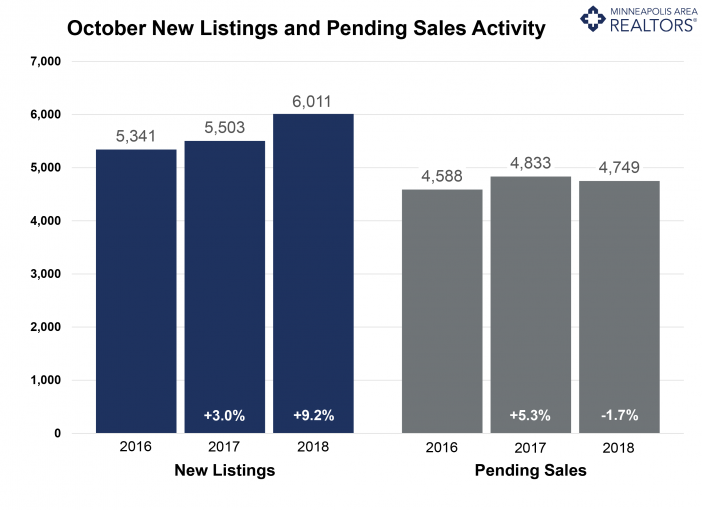

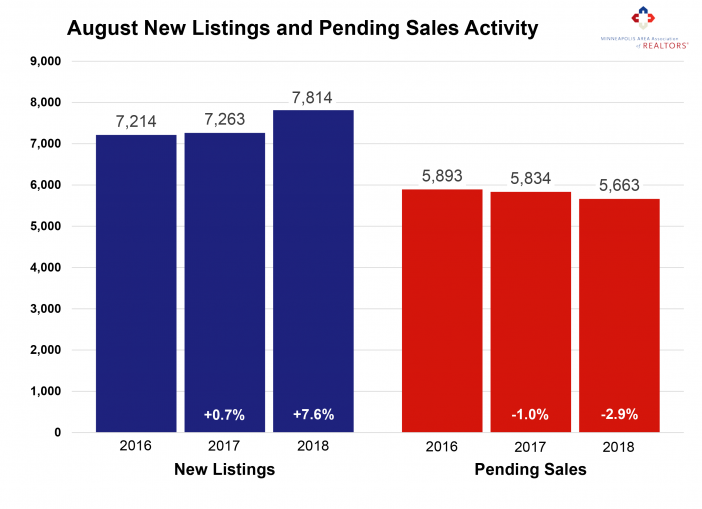

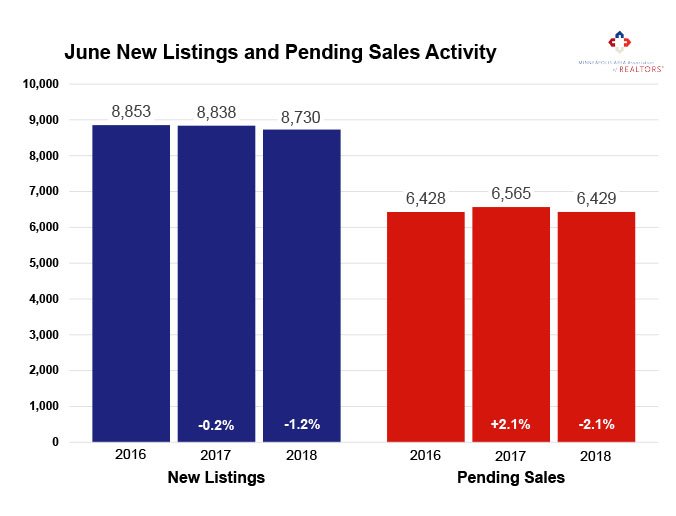

- Sellers listed 6,160 properties on the market, an 8.8 percent decrease from last March

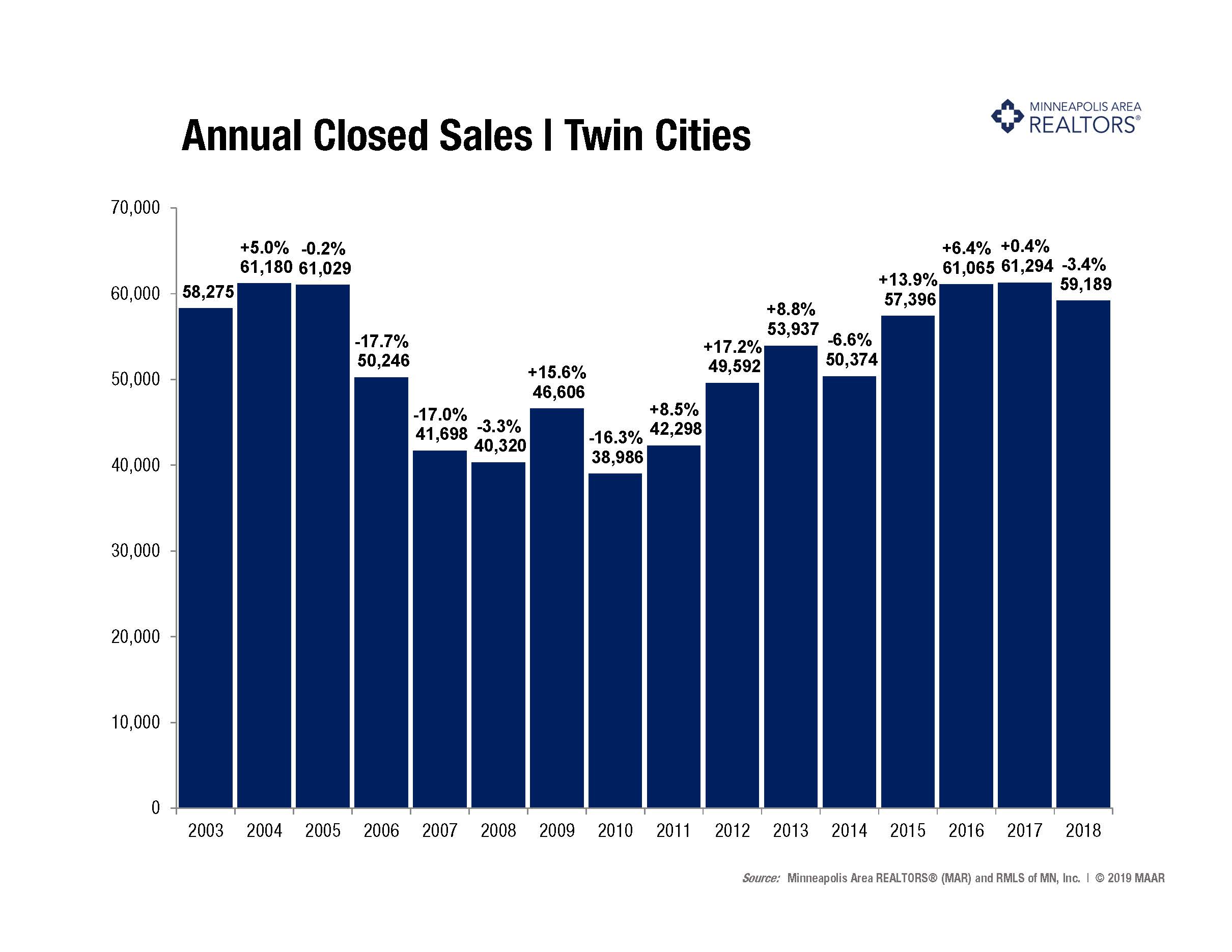

- Buyers closed on 3,673 homes, a 9.3 percent decrease

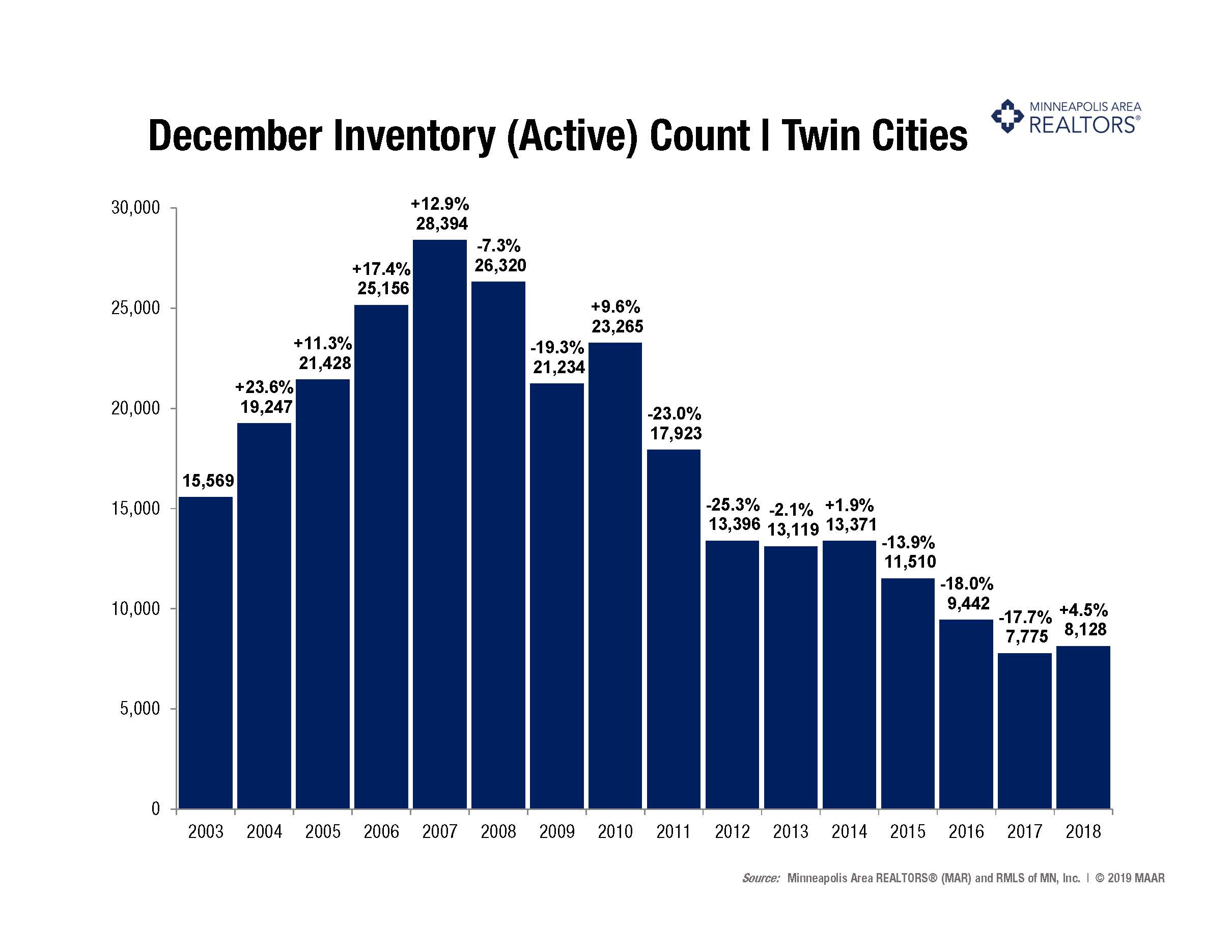

- Inventory levels for March declined 4.2 percent compared to 2018 to 8,685 units

- Months Supply of Inventory was flat at 1.8 months

- “There’s plenty of buyers and sellers out there looking to get deals done,” said Linda Rogers, President-Elect of Minneapolis Area REALTORS®. “If rates and inventory cooperate, we’re still anticipating a solid year.”

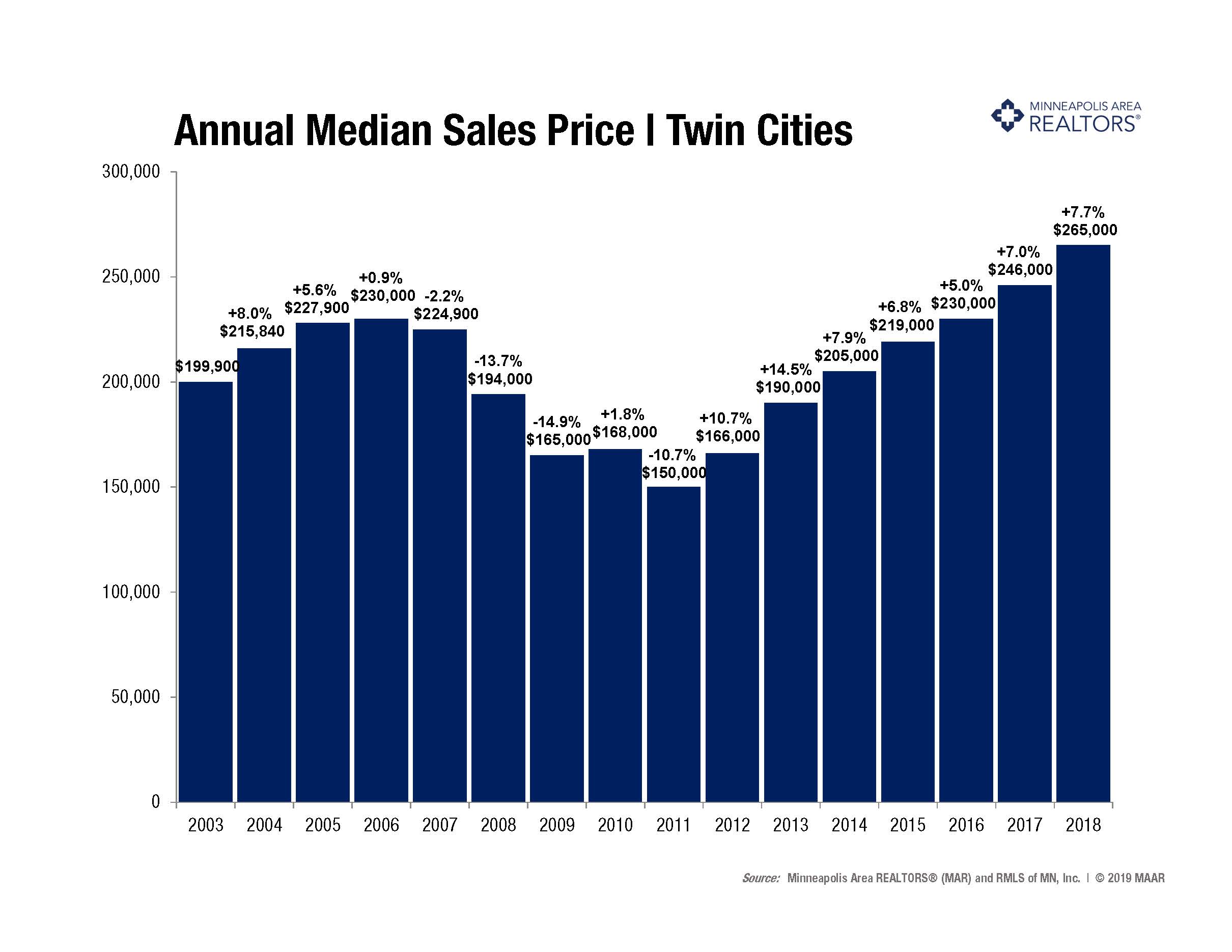

- The Median Sales Price rose 6.5 percent to $275,000, a record high for any month

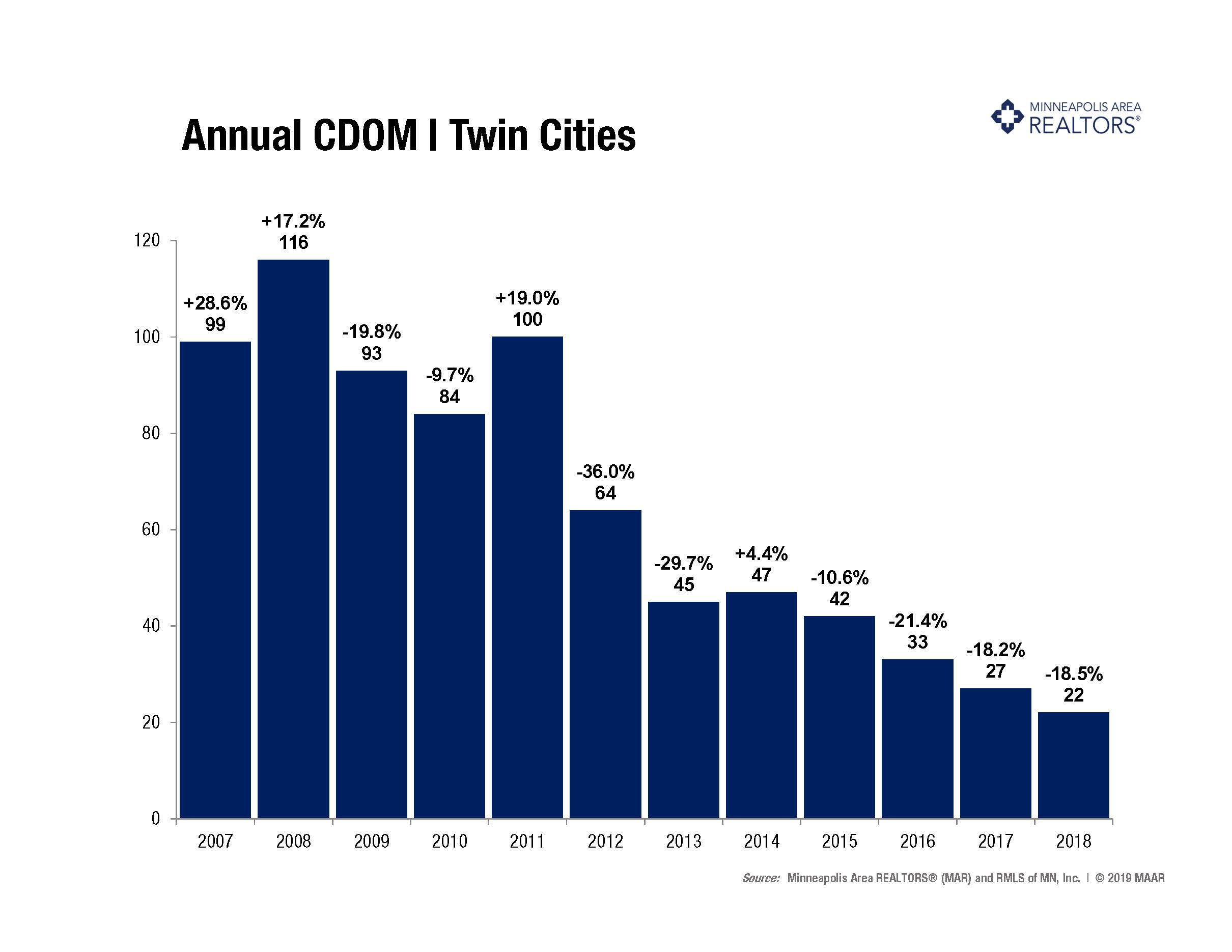

- Cumulative Days on Market rose 15.8 percent to 66 days, on average (median of 30)

- Changes in Sales activity varied by market segment

- Single family sales declined 7.2 percent; condo sales sank 16.5 percent; townhome sales fell 12.2 percent

- Traditional sales decreased 7.9 percent; foreclosure sales declined 26.8 percent; short sales fell 32.3 percent

- Previously-owned sales were down 10.1 percent; new construction sales rose 2.3 percent

Quotables

“The extremes of February and March are still noticeable,” said Todd Urbanski, President of Minneapolis Area REALTORS®. “It’s difficult to disentangle weather-induced market shifts with organic market shifts.”

All information is according to the Minneapolis Area REALTORS® based on data from NorthstarMLS. Minneapolis Area REALTORS® is the leading regional advocate and provider of information services and research on the real estate industry for brokers, real estate professionals and the public. We serve the Twin Cities 16-county metro area and western Wisconsin.

From The Skinny Blog.