New Listings and Pending Sales

Over the past four weeks, the U.S. real estate market entered a typical summer slowdown exacerbated by borrowing pressures as average 30-year fixed mortgage rates spiked to a high of 6.66%. Despite these elevated rates tightening buyer budgets, underlying demand held firm, with pending home sales marking an eighth consecutive month of year-over-year growth at the national level.

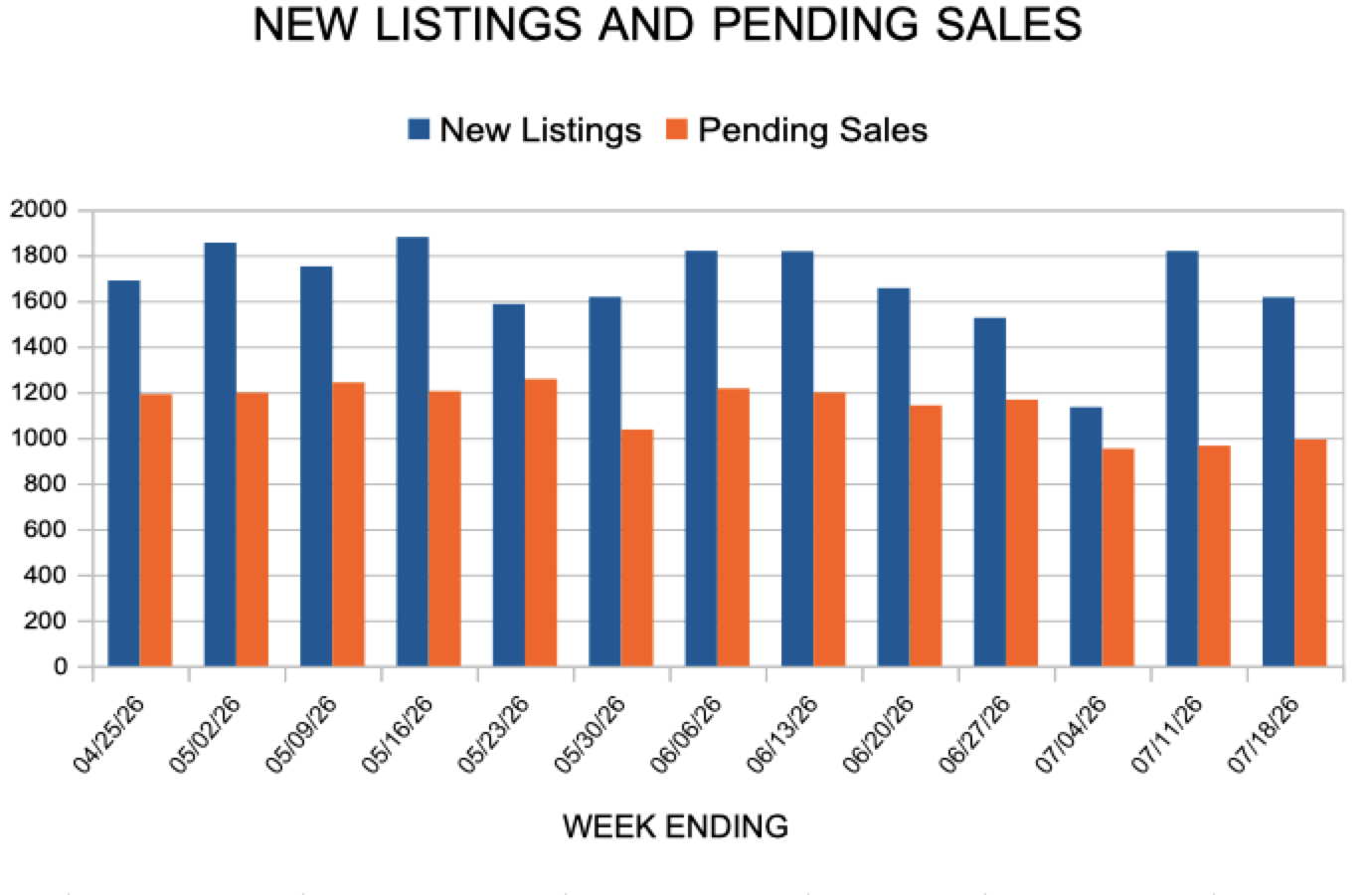

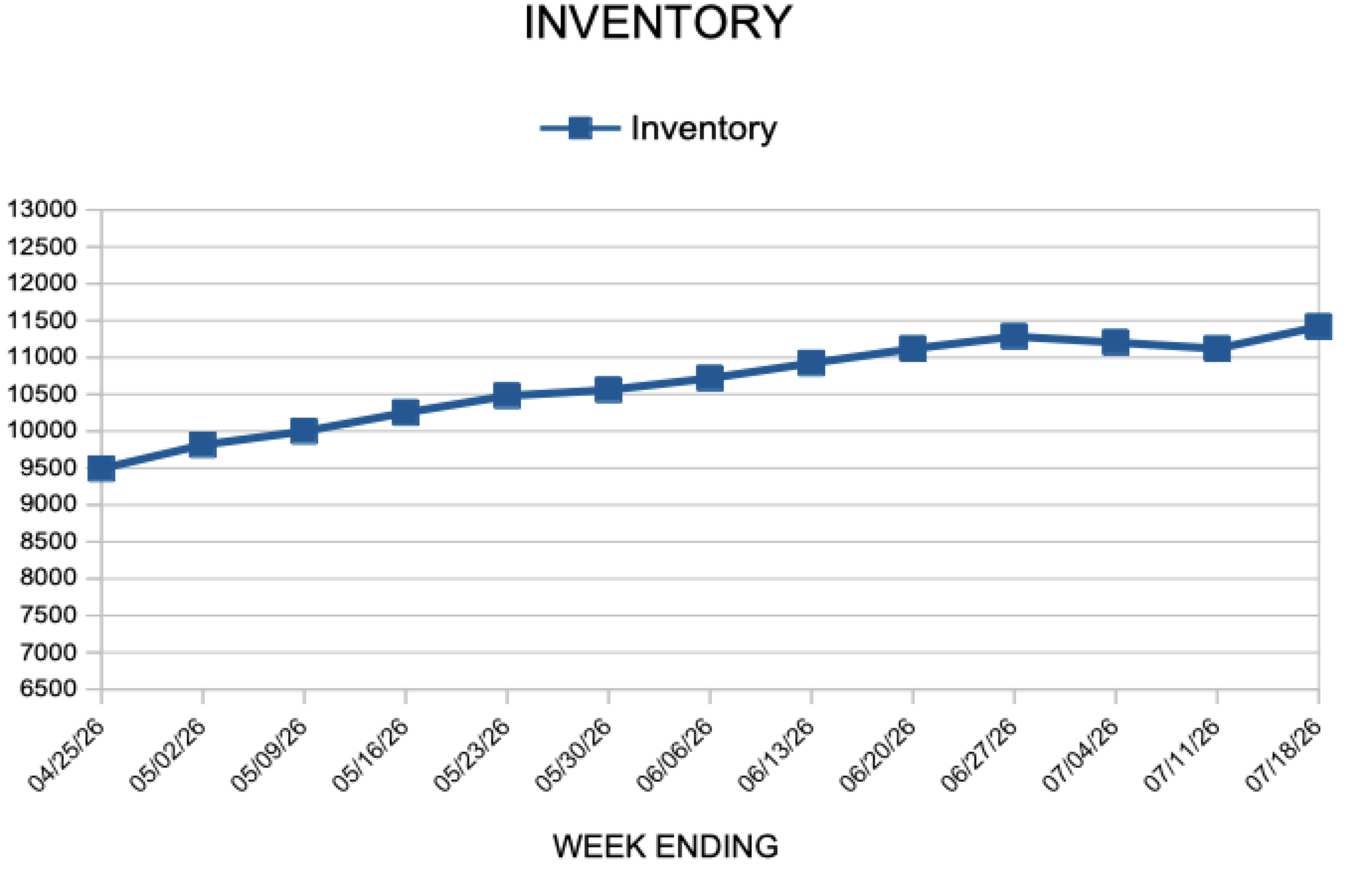

In the Twin Cities region, for the week ending August 1:

For the month of June:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The 30-year fixed-rate mortgage averaged 6.69% this week. While mortgage rates continue to influence affordability, the housing market is showing signs of adjustment, with listing prices modestly below year-ago levels and for-sale inventory improving from the limited supply seen in recent years.

Information provided by Freddie Mac.

As the median age of first-time homebuyers increases, many younger buyers are turning to their parents for financial assistance when purchasing a home. A Veterans United survey found that nearly 6 in 10 parents (59%) have provided or plan to provide financial support to help their children buy a home. Parents assist in a variety of ways, including cash gifts, down payment contributions, and help with closing costs.

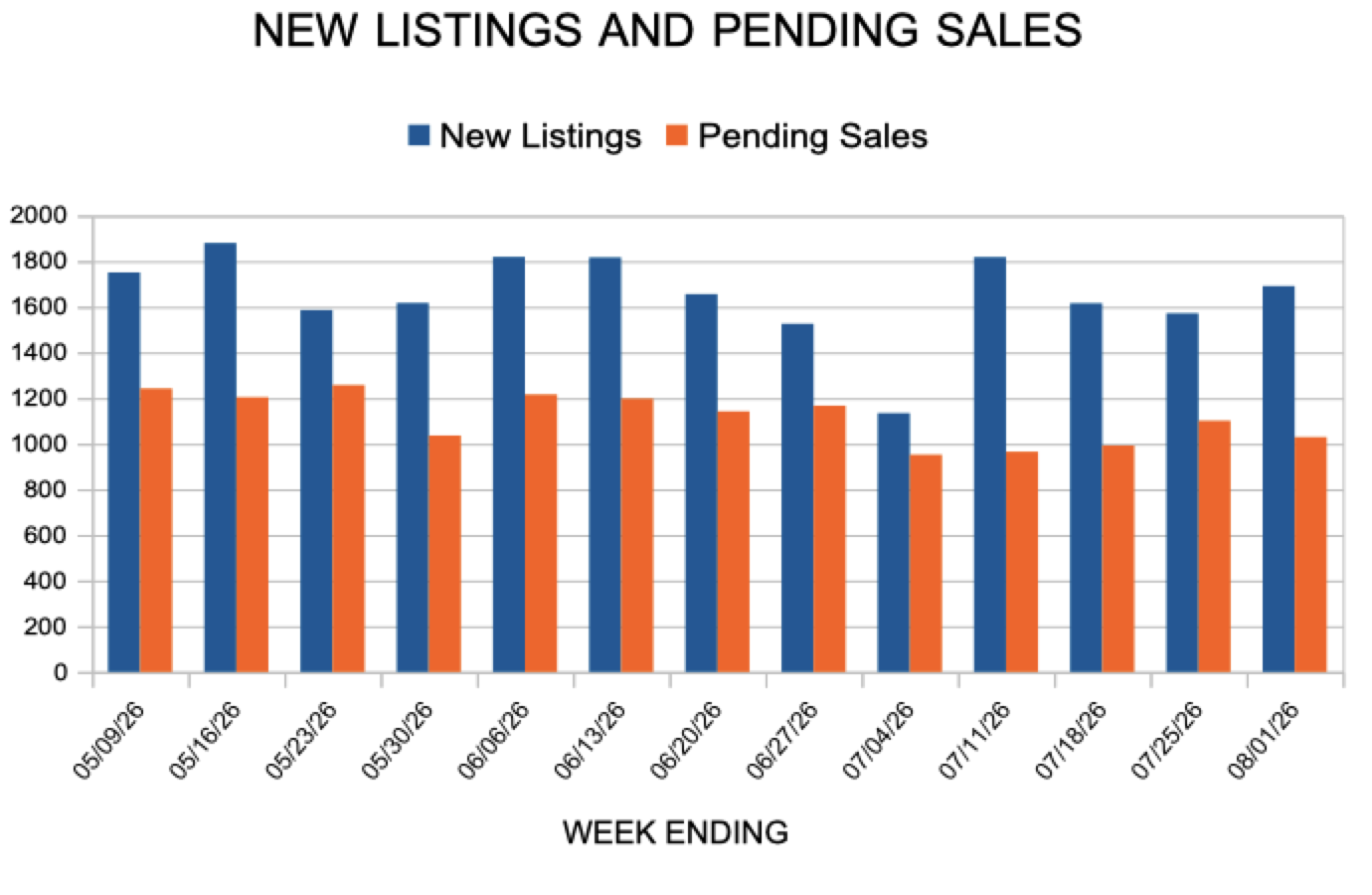

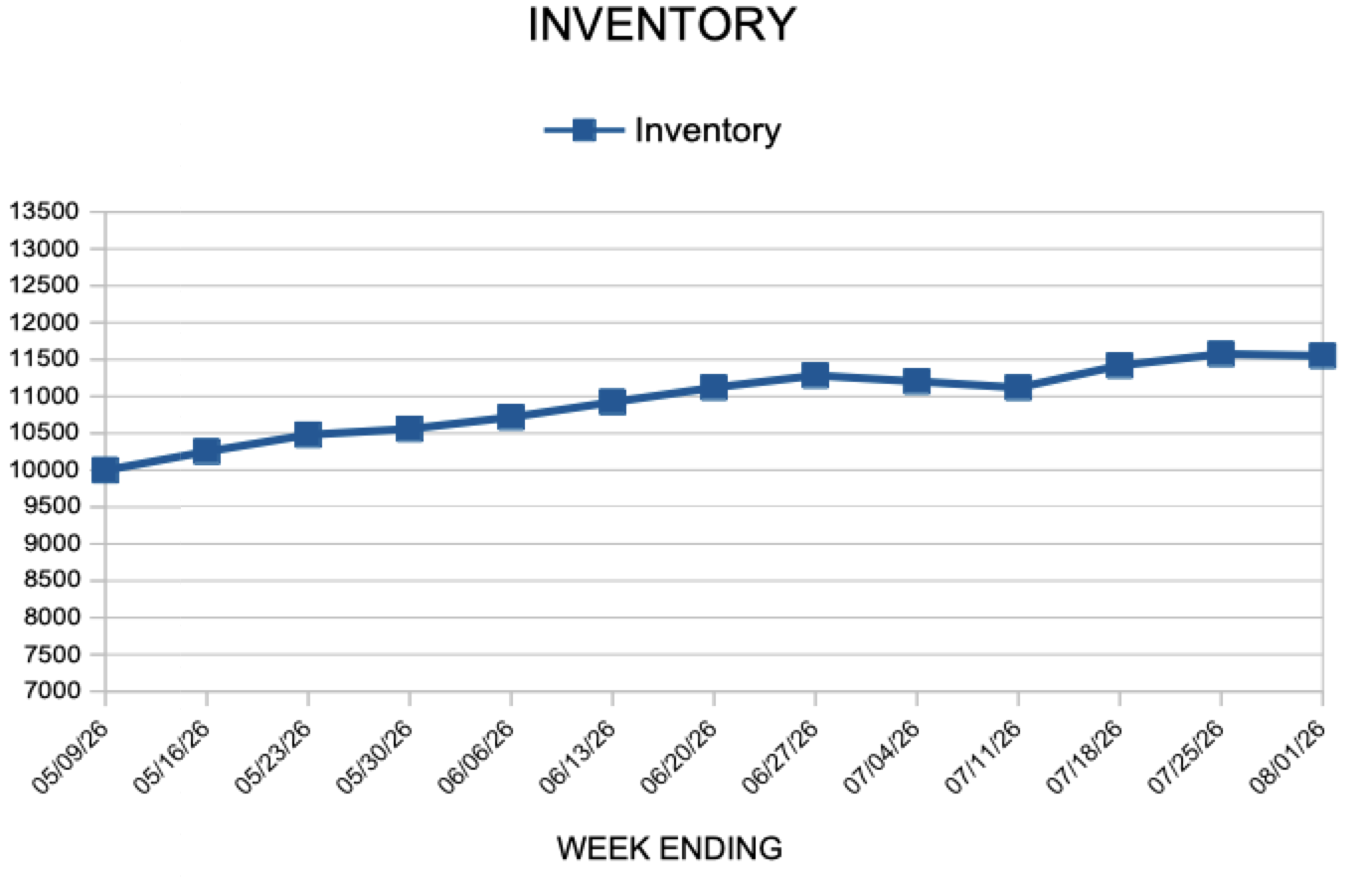

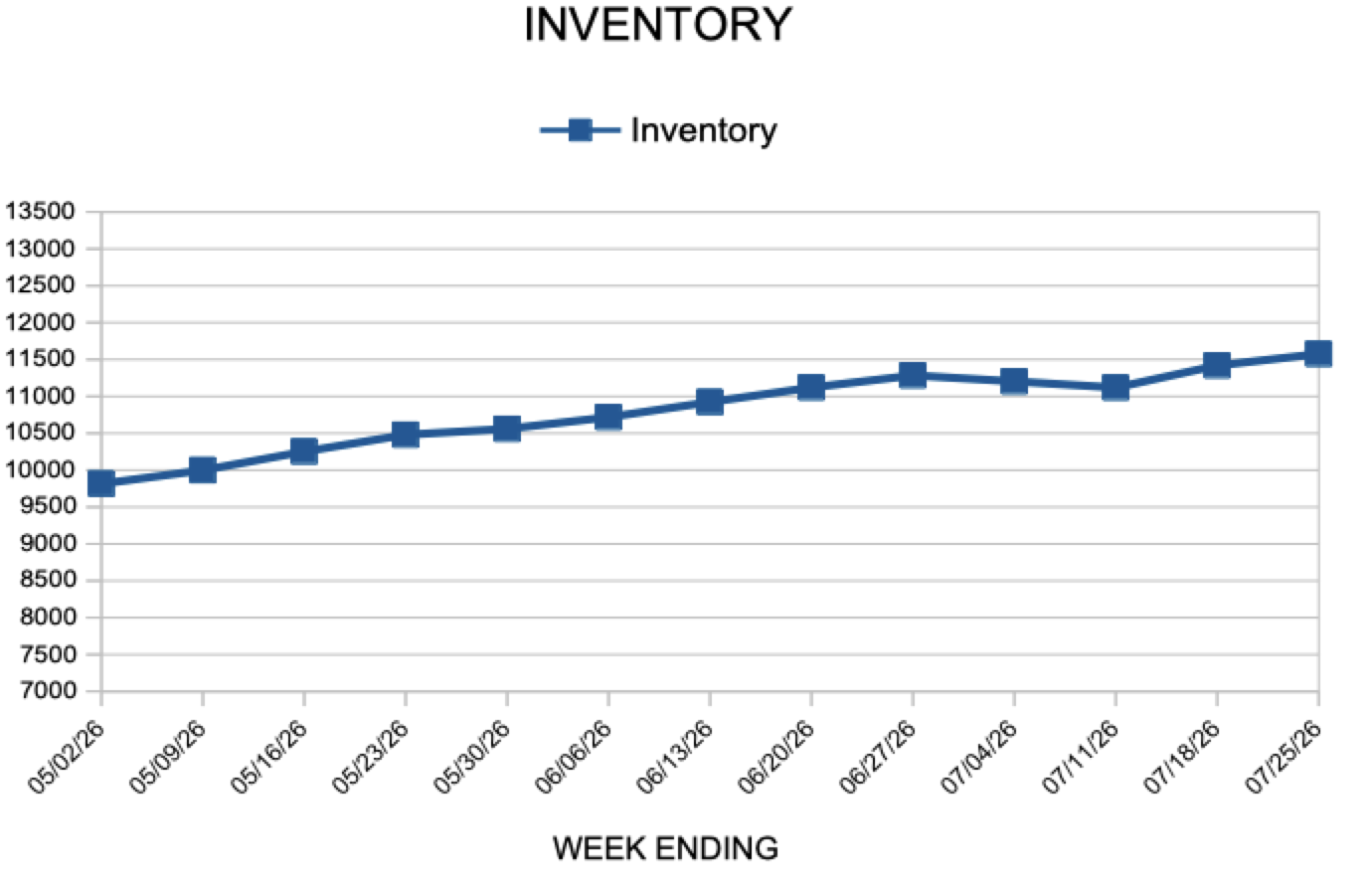

In the Twin Cities region, for the week ending July 25:

For the month of June:

All comparisons are to 2025

Click here for the full Weekly Market Activity Report. From MAAR Market Data News.

The 30-year fixed-rate mortgage averaged 6.66% this week. The housing market continues to benefit from more available inventory, providing prospective homebuyers with additional options and helping support buyer activity as mortgage rates fluctuate.

Information provided by Freddie Mac.