Housing markets have proven to be resilient despite predictions of more challenges this year for housing.

Author Archives: admin

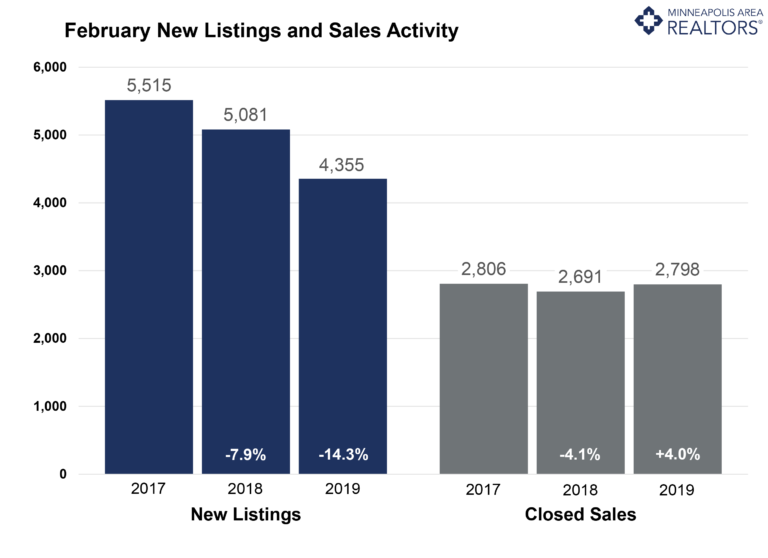

Extreme February Weather Leaves Dent on Residential Market Stats

Winter sports enthusiasts likely enjoyed the snowiest February on record more than those attempting to buy and sell homes. Even so, the latest numbers for Twin Cities residential real estate show some strength amidst ongoing signs of change. Sellers showed a sizeable, weather-related decline in listing activity, while buyers entered into fewer contracts than last February even while closed sales rose. Market times flattened out as the median sales price continued to rise compared to last year. One sign of a changing market is the fact that the ratio of sold to list price has fallen for three of the last four months. This—along with other indicators—suggest the market is improving for buyers, even though sellers still have strong pricing, favorable negotiating leverage and quick market times.

Due to the decline in new listings, the number of active listings for sale decreased compared to the prior year. Even so, buyers have seen inventory gains for four of the last five months. Months supply followed suit, tick down to 1.6 months, suggesting the market is still tight. Buyers should expect competition on the most sought-after listings and neighborhoods. After increasing to 5.0 percent in November, mortgage rates have settled back down around 4.5 percent. That’s great news for buyers. The supply squeeze is most evident at the entry-level prices, where multiple offers and homes selling for over list price are commonplace. The move-up and upper-bracket segments are less competitive and better supplied. Inventory could rise substantially, and we’d still have a balanced market.

February 2019 by the Numbers (compared to a year ago)

Sellers listed 4,355 properties on the market, a 14.3 percent decrease from last February

Buyers closed on 2,798 homes, a 4.0 percent increase

Inventory levels for February declined 5.7 percent compared to 2018 to 7,936 units

Months Supply of Inventory decreased 5.9 percent to 1.6 months

The Median Sales Price rose 6.2 percent to $265,500, a record high for February

Cumulative Days on Market was flat at 69 days, on average (median of 43)

Changes in Sales activity varied by market segment

Single family sales rose 6.7 percent; condo sales fell 0.9 percent; townhome sales increased 1.0 percent

Traditional sales increased 7.4 percent; foreclosure sales sank 40.3 percent; short sales fell 41.4 percent

Previously-owned sales were up 4.7 percent; new construction sales rose 5.3 percent

Quotables

“The cold and snow in February was certainly an impediment,” said Todd Urbanski, President of Minneapolis Area REALTORS®. “The March numbers will offer more clarity on market direction.”

“We’re still sensing plenty of interest from buyers and sellers,” said Linda Rogers, President-Elect of Minneapolis Area REALTORS®. “This spring market should be productive, especially with more inventory.”

All information is according to the Minneapolis Area REALTORS® based on data from NorthstarMLS. Minneapolis Area REALTORS® is the leading regional advocate and provider of information services and research on the real estate industry for brokers, real estate professionals and the public. We serve the Twin Cities 16-county metro area and western Wisconsin.

From The Skinny Blog.

Weekly Market Report

For Week Ending March 9, 2019

New listings and overall housing inventory are still proceeding slower than last year in many markets across the U.S., and they are mostly trailing activity for last year, which was already rather low. Sales have also been slower than last year at this time in areas with lingering winter weather, but the thaw is on. That may present a new set of difficulties for communities that have experienced an abundance of rain and snow over the last few months.

In the Twin Cities region, for the week ending March 9:

- New Listings decreased 8.6% to 1,304

- Pending Sales decreased 16.2% to 917

- Inventory decreased 6.2% to 8,117

For the month of February:

- Median Sales Price increased 6.2% to $265,500

- Days on Market remained flat at 69

- Percent of Original List Price Received decreased 0.3% to 97.7%

- Months Supply of Homes For Sale remained flat at 1.7

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

Weekly Market Report

For Week Ending March 2, 2019

Sales totals have been mixed across the nation and dependent on what has been a considerably persistent wintry mix in the Great Plains, Midwest and Northeast. While this time of year brings unpleasant weather to all parts of the country, it has less impact on southern and western states. While there is no true national real estate market, overarching trends continue to be higher prices and more inventory, especially west of the Rocky Mountains. Let’s look more closely at what is happening locally.

In the Twin Cities region, for the week ending March 2:

- New Listings decreased 20.0% to 1,257

- Pending Sales decreased 13.3% to 923

- Inventory decreased 5.5% to 8,009

For the month of January:

- Median Sales Price increased 6.1% to $259,000

- Days on Market decreased 5.8% to 65

- Percent of Original List Price Received increased 0.1% to 97.0%

- Months Supply of Homes For Sale increased 13.3% to 1.7

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

Weekly Market Report

For Week Ending February 23, 2019

Two years ago, Millennials (born between 1981 and 1996) passed older generational groups to account for the most new mortgages. Today, Millennials also account for the most total dollar amount of those mortgages. Given the state of ongoing median sales price increases in the majority of the country, this should not come as a surprise. And given the positive state of the U.S. economy, finding the correct balance between positive sales figures and sales prices will be a dominant theme of 2019.

In the Twin Cities region, for the week ending February 23:

- New Listings decreased 25.0% to 949

- Pending Sales decreased 12.6% to 866

- Inventory decreased 3.0% to 8,093

For the month of January:

- Median Sales Price increased 6.1% to $259,000

- Days on Market decreased 5.8% to 65

- Percent of Original List Price Received increased 0.1% to 97.0%

- Months Supply of Homes For Sale increased 13.3% to 1.7

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

Weekly Market Report

For Week Ending February 16, 2019

The National Association of REALTORS® has reported in the last month that national existing-home sales and pending sales are both down in year-over-year comparisons, but that has not necessarily been a constant from market to market. While weather-related events have hampered some of the necessary machinations of making home sales, buyers have shown determination toward achieving their homeownership goals. This week has shown some sales strain in many markets, but spring is just around the corner.

In the Twin Cities region, for the week ending February 16:

- New Listings decreased 20.5% to 1,018

- Pending Sales decreased 10.5% to 810

- Inventory decreased 2.5% to 8,043

For the month of January:

- Median Sales Price increased 6.1% to $259,000

- Days on Market decreased 5.8% to 65

- Percent of Original List Price Received increased 0.1% to 97.0%

- Months Supply of Homes For Sale increased 13.3% to 1.7

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

A mostly strong start to the year

By David Arbit on Tuesday, February 19th, 2019

The latest numbers show that 2019 was off to a good start for TwinCities residential real estate. Sellers produced another increase in listing activity, while buyers entered into more contracts than last January even while closed sales fell. Market times continued to shrink as the median sold home price rose compared to last year. After two months of declines, the ratio of sold to list price rose slightly in January. There are some early indications the market is improving for buyers, even though sellers still have strong negotiating leverage and quick market times.

The number of active listings for sale has increased compared to the prior year. Buyers have seen inventory gains for four consecutive months. Months supply also ticked up to 1.6 months, suggesting the market is still tight but rebalancing and normalizing. After increasing to 5.0 percent in November, mortgage rates have settled back down around 4.5 percent. The lack of supply is especially noticeable at the entry-level prices, where multiple offers and homes selling for over list price are commonplace. The move-up and upper-bracket segments are less competitive and better supplied. Inventory could rise substantially, and we’d still have a balanced market.

January 2019 by the Numbers

(compared to a year ago)

– Sellers listed 4,359 properties on the market, a 7.8 percent increase from last January

– Buyers closed on 2,681 homes, a 4.6 percent decrease

– Inventory levels for January rose 1.1 percent compared to 2018 to 7,828 units

– Months Supply of Inventory increased 6.7 percent to 1.6 months

– The Median Sales Price rose 6.1 percent to $258,900, a record high for January

– Cumulative Days on Market declined 5.8 percent to 65 days, on average (median of 44)

– Changes in Sales activity varied by market segment:

– Single family sales fell 5.2 percent; condo sales rose 5.3 percent; townhome sales declined 2.9 percent

– Traditional sales decreased 1.4 percent; foreclosure sales sank 50.3 percent; short sales were flat

– Previously-owned sales were down 5.5 percent; new construction sales ramped up by 12.8 percent

Quotables

“We’re still very much undersupplied locally and nationally,” said Todd Urbanski, President of Minneapolis Area REALTORS®. “We’re expecting 2019 to be a good year for both buyers and sellers.”

“Our data shows slightly more inventory, and rates are down from where they were at the end of last year,” said Linda Rogers, President-Elect of Minneapolis Area REALTORS®. “Buyers should know that they’re going to find more options out there this spring and summer.”

All information is according to the Minneapolis Area REALTORS® based on data from NorthstarMLS. Minneapolis Area REALTORS® is the leading regional advocate and provider of information services and research on the real estate industry for brokers, real estate professionals and the public. We serve the Twin Cities 16-county metro area and western Wisconsin.

From The Skinny Blog.

January Monthly Skinny Video

“Despite a strong U.S. economy, historically low unemployment and steady wage growth, home sales began to slow across the nation in late last year.”

Weekly Market Report

For Week Ending February 9, 2019

For the third of four weeks, it is worthwhile to mention the weather when discussing residential real estate in large portions of the U.S. After a relatively quiet December and January, February has turned in some impressively cold and snowy days that have stalled some buying and selling actions. That said, housing markets are proving to be resilient in the face of predictions of a tougher year for the industry. It’s early, but economic fundamentals remain positive.

In the Twin Cities region, for the week ending February 9:

- New Listings decreased 17.4% to 1,135

- Pending Sales decreased 13.9% to 765

- Inventory increased 1.2% to 7,966

For the month of January:

- Median Sales Price increased 6.1% to $259,000

- Days on Market decreased 5.8% to 65

- Percent of Original List Price Received increased 0.1% to 97.0%

- Months Supply of Inventory increased 6.7% to 1.6

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.

Weekly Market Report

For Week Ending February 2, 2019

Despite weather events that have brought frigid temperatures and heavy snow to large swaths of the U.S., residential real estate markets have performed better than anticipated so far this year. While a complete downturn in sales and prices was not at all expected, some softening was anticipated. Instead, pending sales are performing well in many markets, while new listings are not experiencing any negative swings of concern.

In the Twin Cities region, for the week ending February 2:

- New Listings decreased 9.2% to 912

- Pending Sales increased 4.4% to 834

- Inventory increased 2.6% to 8,023

For the month of December:

- Median Sales Price increased 4.0% to $258,000

- Days on Market decreased 6.6% to 57

- Percent of Original List Price Received decreased 0.2% to 96.9%

- Months Supply of Inventory increased 13.3% to 1.7

All comparisons are to 2018

Click here for the full Weekly Market Activity Report. From The Skinny Blog.