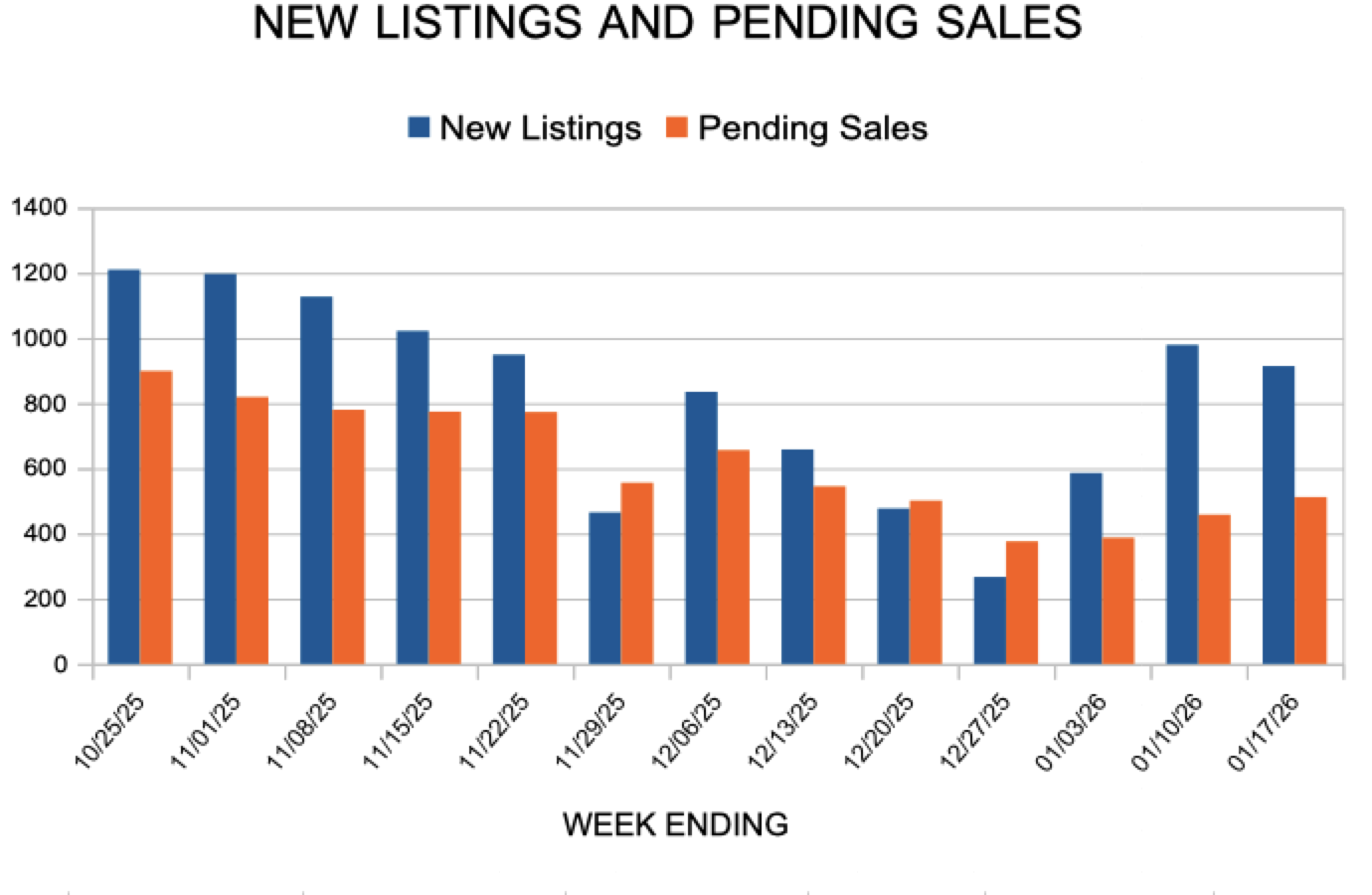

Minneapolis, Minnesota (July 12, 2012) – The empirical evidence of a market in recovery is beginning to accumulate. Sales counts and prices are up; inventory and months of supply are down. In June 2012, buyers signed 4,917 purchase agreements, 16.0 percent higher than June 2011.

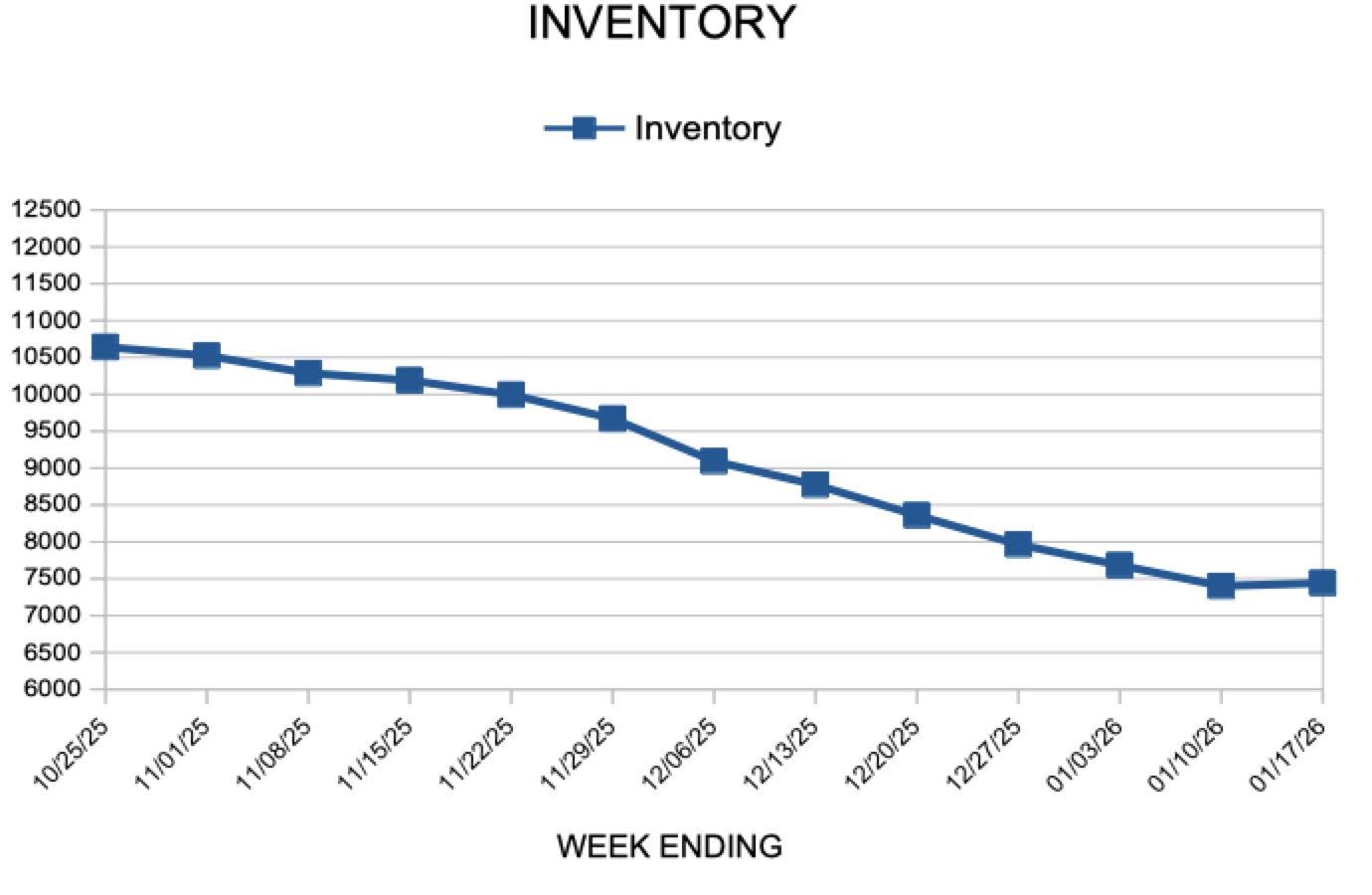

Sellers introduced 6,359 properties to the market, 8.1 percent fewer than last June. The number of homes for sale has dropped for 17 consecutive months, down 31.2 percent from last year to 17,103 active listings – the lowest inventory reading for any month since January 2004. Months’ supply of inventory dropped 44.6 percent to 4.4 months – the lowest reading for any month since December 2005.

The median sales price rose 10.7 percent to $179,500. That’s the second-largest gain since January 2004 and the fourth consecutive month of year-over-year gains. Excluding only June 2010, home prices are at their highest level since October 2008.

Homes sold in 113 days, on average, down 22.0 percent from last year. Sellers received an average of 95.1 percent of their list price, up 4.0 percent from last year. Cash buyers made up 19.3 percent of all closed sales.

“It’s difficult to find a negative trend in the local housing market right now,” said Cari Linn, President of the Minneapolis Area Association of REALTORS® (MAAR). “After many years of decline, it’s a welcome change of pace.”

One catalyst enabling these trends is the declining role of lender-mediated market activity, also known as distressed sales (foreclosures and short sales)

Distressed sales accounted for 30.6 percent of all new listings and 34.6 percent of all closed sales, the lowest shares since June 2008 and August 2008, respectively.

Looking at price movement by market segment, traditional median home prices were up 3.4 percent to $215,000, foreclosure prices were up 10.5 percent to $124,700 and short sales were down 2.7 percent to $126,500. Traditional homes sold for nearly 75.0 percent more than foreclosures and accounted for 65.4 percent of sales volumes, highlighting the importance of market share relative to overall market median sales price.

“This is what we hoped to see with distressed sales,” said Andy Fazendin, MAAR President-Elect. “Now we just need to get traditional inventory in line with buyer demand. With rents on the rise and mortgage rates maintaining at historical lows, potential sellers should take note.”

All information is according to the Minneapolis Area Association of REALTORS® (MAAR) based on data from the Regional Multiple Listing Service of Minnesota, Inc. MAAR is the leading regional advocate and provider of information services and research on the real estate industry for brokers, real estate professionals and the public. MAAR serves the Twin Cities 13-county metro area and western Wisconsin.

Read it on The Skinny

For Week Ending January 10, 2026

For Week Ending January 10, 2026